India’s farmers are the backbone of the country’s economy—yet cheap credit is one of their largest problems. With a view to bridging this gap, the Government of India, with the help of the Reserve Bank of India (RBI) and NABARD, introduced the Kisan Credit Card (KCC) scheme. This revolutionary program extends farmers timely and convenient credit for farm and allied operations—be it growing crops, rearing animals, or fisheries.

But despite millions of people benefiting through the KCC scheme, there are many who still find the application procedure complex. We will guide you through the entire Kisan Credit Card loan application process in 2025—from eligibility to documents, and approval to disbursement—with all the details you need to make your loan procedure smooth and successful.

What is a Kisan Credit Card (KCC)?

The Kisan Credit Card is a revolving credit facility of short-term duration designed for farmers. It gives them easy access to cheap, collateral-free credit for agricultural and allied operations such as cultivation of crops, dairy, poultry, fisheries, and even buying of farm tools.

Established in 1998, the program has over the years been revised and today provides interest subvention benefits, soft repayment terms, and even accidental death or disability insurance. The KCC program remains one of India’s best rural credit innovations to date in 2025.

Why KCC is a Game-Changer for Farmers

The biggest plus of the KCC is that it makes finance easily accessible. Farmers are no longer dependent on moneylenders and other informal credit providers. They can borrow working capital from banks directly at interest rates from a minimum of as low as 4% per annum (under government interest subvention).

It can be utilized as a debit card—for repayment, withdrawal, and transaction directly from bank branches or ATMs. The farmer is allowed to borrow up to a pre-approved limit based on his landholding, cropping pattern, and capacity to repay.

Overall, the Kisan Credit Card is a lifeline of finance, providing liquidity, infusing self-reliance, and nurturing sustainable agriculture.

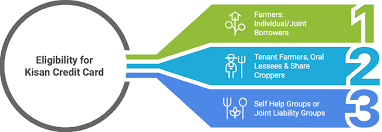

Eligibility for KCC Loan

The Kisan Credit Card loan is extended to numerous rural beneficiaries, including the non-traditional farmers.

The following are eligible:

Individual farmers who own or hold farms in agricultural land individually or on lease.

Tenant farmers and sharecroppers.

Self-help groups (SHGs) and joint liability groups (JLGs).

Fishermen, dairy farmers, poultry farmers, and other livestock keepers.

Small and marginal farmers engaged in allied farm enterprises such as sericulture, horticulture, or floriculture.

The government has also made it inclusive in 2025 so that even landless farmers and small farmers can benefit through joint liability schemes.

Step-by-Step KCC Loan Application Process

Getting a loan from a Kisan Credit Card is simple if you follow step by step. This is how you can do it in a simple way:

The procedure of getting a Kisan Credit Card loan is easy if you follow step by step. Let’s break it down briefly:

Step 1: Select Your Bank

You can get a KCC loan from any nationalized bank, regional rural bank (RRB), cooperative bank, or a few private sector banks. SBI, HDFC, Bank of Baroda, and Axis Bank are some well-known banks that fall under the scheme.

The farmers can submit their forms in bank branches, Common Service Centres (CSCs), or online through the bank’s official websites and NABARD’s KCC portal.

Step 2: Fill in the KCC Application Form

Get the Kisan Credit Card Application Form from the bank or download it from the bank’s website. The form asks for details such as

Personal information (name, address, Aadhaar, PAN, etc.)

Farm information (landholding, pattern of crops, type of irrigation)

Loan needed and purpose

Repayment preference and security provided (if any)

Cross-check all the information twice because any error can lead to a delay in approval.

Step 3: Attach Mandatory Documents

Fill and submit the form along with the documents. The common documents required are

Identity proof: Aadhaar card, PAN card, or voter ID card

Address proof: Utility bill or ration card

Land ownership proof: 7/12 extract, lease agreement, or land record certificate

Photograph: Recent passport-size photo

Bank account details: Latest bank passbook or account statement

Income proof or crop information can even be requested by certain banks to verify eligibility.

Step 4: Verification at Bank and Farm

The bank verifies once your application and documents have been submitted. This involves a credit record, land ownership, and agricultural activity verification. A field officer or agriculture officer typically visits the farm for verification in most instances.

This step ensures that the sanctioned amount of the loan matches with the true size of the land, cropping pattern, and yield level.

Step 5: Sanction of Loan and Issue of KCC

Once your application is accepted, the bank will sanction the loan and provide your Kisan Credit Card that will serve as an ATM-cum-debit card as well as a credit facility.

Credit limit is fixed against varied parameters—crop type, area, water source, and repayment history. The card is valid for 3 to 5 years, renewable every year, and subject to annual review.

Once you have the card, you can withdraw cash, buy inputs, or pay dues as and when you need it.

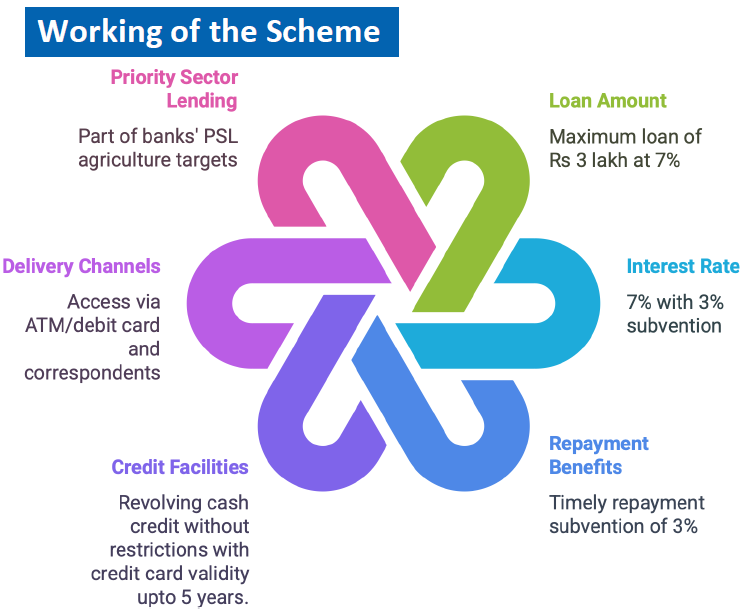

KCC Loan Amount and Interest Rates

KCC loan amounts generally range from ₹10,000 to ₹3 lakh in agriculture, although they can go up to ₹10 lakh for allied operations such as dairy or fisheries.

Interest rates are bank-specific but generally between 7% and 9% per year. With government subvention of interest, premature repayment could reduce the effective rate to as low as 4%.

Further, the Pradhan Mantri Fasal Bima Yojana (PMFBY) insures KCC holders for crop loss due to natural disasters or infestation.

Digital KCC Application (Online Process)

Banks have made the KCC process digitalized in 2025 to make transactions faster and more transparent. Farmers can apply online by:

Official bank websites (SBI, HDFC, PNB, etc.)

NABARD’s KCC Portal

Common Service Centres (CSC Kisan Portal)

By uploading papers online and undertaking e-KYC verification, farmers can minimize paperwork and take advantage of clearances earlier.

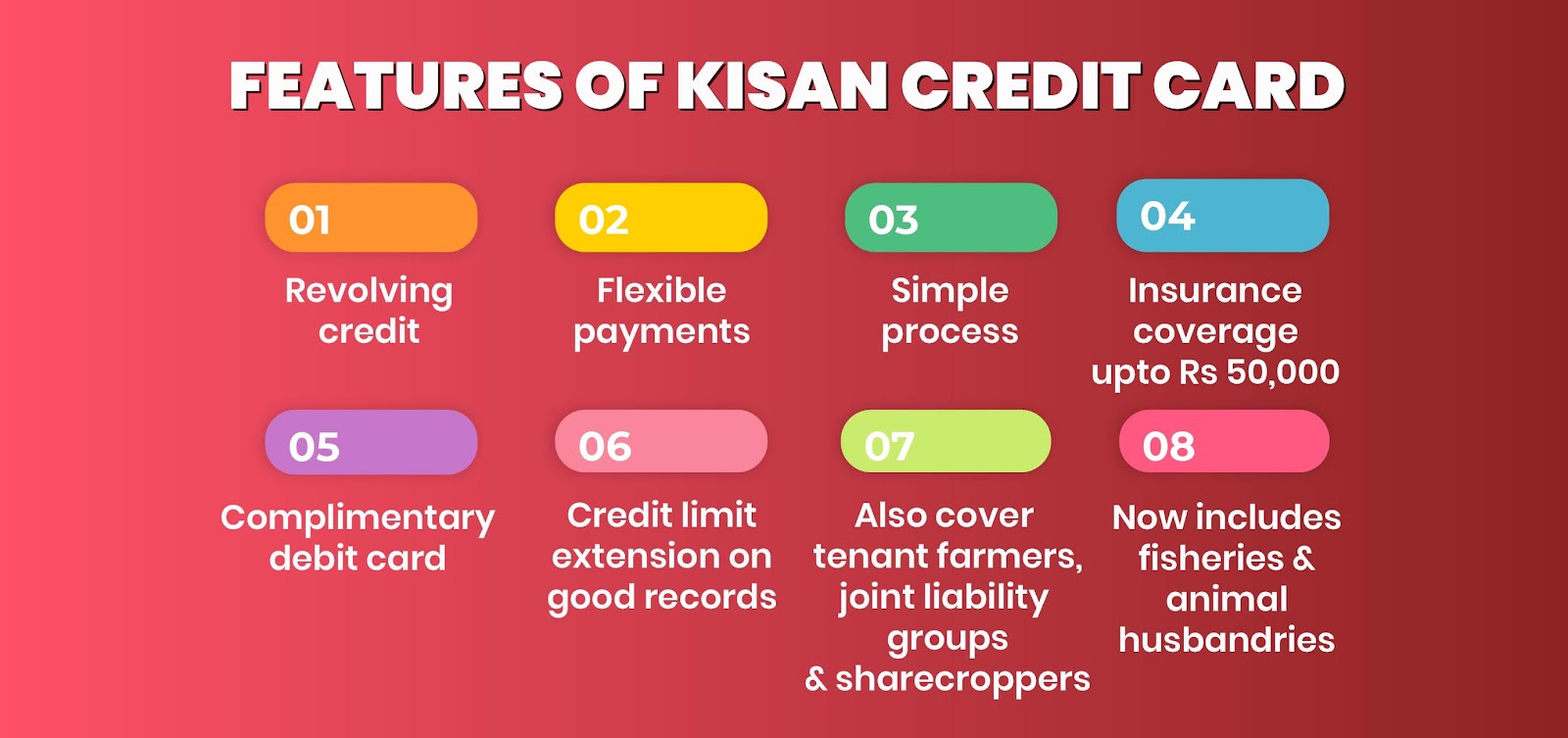

Advantages of the KCC Scheme

The Kisan Credit Card is not a credit; it’s a doorway to economic empowerment. Here’s why it matters:

Easy access to cheap credit without moneylenders.

Farming repayment durations overlap durations of harvesting crops.

Low cost of interest due to government subsidy.

Inclusive coverage covering allied industries such as dairy, fishery, and horticulture.

Crop and farmer insurance coverage.

Extensive acceptability and interoperability via banking channels.

True in a very literal sense, the KCC turns farmers into entrepreneurs—making them liquid, more productive, and resilient.

Common Mistakes to be Avoided

The majority of farmers are disqualified due to incomplete forms or unsuitable information provided in the application form. Prevent mistakes by thoroughly double-verifying each input, keeping your land documents current, and submitting accurate crop information.

Delays happen when the applicants fail to satisfy the bank’s Know Your Customer (KYC) or e-KYC criteria. Preparing these steps in advance can, in reality, save valuable time.

The Kisan Credit Card scheme is still one of the best monetary instruments for India’s farmers—allowing them to plan, invest, and prosper with confidence. In 2025, the digitalization of KCC has accelerated the process to become faster, easier, and more convenient than ever before.

For the farmer who wishes to grow his farm, invest in livestock, or mechanize his farm, the KCC is not just a credit card—it’s an investment in progress and prosperity.

Therefore, if you have not yet applied for a KCC, now is the time. Go to your nearest bank branch or apply online, and take that fearless step towards financial freedom and farm growth.